What PE Firms Miss When Technical Diligence Gets One Paragraph

Private equity firms reprice financial risk all the time, but technical risk often gets reduced to a short paragraph in the investment committee memo. That can be expensive.

A software platform may look stable during the deal process while hiding immature AI features, untested scalability, key-person dependency, roadmap pressure, and architectural limits that only become visible after close.

If your firm is evaluating a software company or software-enabled acquisition and needs to understand whether the platform can support the investment thesis, Sharp Logica can help with an executive-level Technical Due Diligence Assessment, including platform risk, scalability, engineering capacity, roadmap credibility, and post-close remediation priorities. You can book a 30-min free call, view the services, or email us at info@sharplogica.com with specific questions.

Introduction

Private equity firms usually know how to handle financial risk once it becomes visible. If revenue quality is weaker than expected, if churn is higher than the seller suggested, or if margins depend on savings that will not survive ownership, the model changes. The deal team has familiar tools for those situations: valuation adjustments, different terms, earnouts, changes to debt assumptions, or, in some cases, a decision not to proceed.

Technical risk often receives less precise treatment, even when the target is a software company or a software-enabled business. It may be reviewed, acknowledged, and summarized for the investment committee, but it is too often compressed into a short paragraph that effectively says the platform works today and any weaknesses can be handled after close. That assumption may be reasonable for minor issues, but it becomes dangerous when the investment thesis depends on product expansion, margin improvement, enterprise readiness, AI capability, or faster delivery.

A company can look healthy during the deal process while still carrying technical risk that has not yet become visible. The product demo may be polished, customers may be renewing, and management may explain the roadmap with confidence. The platform may even perform well at the current customer count. None of that proves the system can support the growth plan being underwritten.

In many diligence situations, the gap appears between the story presented before close and the operating reality the buyer inherits afterward. AI features shown in the pitch may not reflect what is actually running in production. A platform that works at today's volume may never have been tested at three times the load. An engineering team may look stable from the outside while one or two people quietly hold together the deployment process, the data model, or the customer integrations that nobody else fully understands.

By the time those issues become obvious, valuation is often locked and the 100-day plan is already underway. The operating partner is no longer dealing with a diligence question. The issue has become part of the ownership agenda.

The risk is not always visible before close

Most management presentations show the company at its best. That is normal in any sale process, and it does not automatically mean the seller is hiding something. The more practical problem is that the version of the product shown to buyers is often cleaner than the operating reality behind it.

This is especially true when AI appears in the product story. In one company, an "AI-enabled workflow" may mean a production capability with monitoring, feedback loops, controlled data handling, and measurable performance. In another, it may mean a prototype connected to a manual review queue, with a senior engineer or operations person fixing failed cases before the customer sees them. Both can look credible in a demo, but they create very different ownership risks.

Scalability can create the same kind of false comfort. A platform may perform well in the current environment while hiding constraints in the database, reporting layer, background jobs, tenant isolation model, or third-party integrations. Cloud hosting can make the infrastructure look modern, but it does not make the architecture scalable by itself. In some cases, it only makes inefficient design more expensive to operate.

Roadmaps also need to be read carefully. They usually describe what the company wants to build, not what the engineering organization can realistically deliver under current conditions. If most capacity is already being consumed by maintenance, customer escalations, fragile integrations, and quality issues, the roadmap is not yet a plan. It is a statement of intent that still has to survive contact with the platform and the team that will be asked to deliver it.

The diligence question is therefore narrower and more useful than a generic review of the technology estate. It asks whether the system underneath the business can support the next phase of growth without forcing a painful reset after close.

The IC memo can make technical risk look smaller than it is

Technical risk usually becomes visible to investors in summarized form. A few findings are listed, a few mitigations are noted, and the overall conclusion often says that the issues are manageable. That may be enough when the risks are genuinely limited, but it can also create a false sense of containment.

Every real platform carries debt, shortcuts, old decisions, and areas that need cleanup, so most technical weaknesses should not dominate the deal discussion. The real question is whether any of those weaknesses change the economics, timing, or execution risk of the investment plan.

For a PE deal team, the useful question is not whether the architecture would satisfy an engineer's ideal design preferences. The useful question is whether the platform can support the commercial plan without forcing the first year of ownership to become a stabilization exercise. If that is uncertain, the IC memo should not treat the risk as background noise.

This is where technical risk is harder to handle than many financial risks. Once a financial issue is visible, it can often be modeled directly. Technical risk usually has to be translated before it can influence valuation, operating planning, or governance. A fragile deployment process becomes a release predictability problem. Weak tenant isolation becomes an enterprise-readiness problem. Poor observability becomes an operational-control problem. Concentrated knowledge becomes a transition-risk problem.

If that translation does not happen before close, the buyer inherits uncertainty rather than a bounded risk.

The same ownership problems keep appearing

In software deals, technical problems rarely appear as one dramatic failure. They usually show up as a set of connected weaknesses that accumulated while the company was growing. The team made practical compromises under customer pressure, shipped features quickly, added integrations, and normalized workarounds because there was always another customer commitment or sales opportunity in front of them. Those compromises are understandable, which is why diligence has to separate normal operating debt from risks that can change the ownership plan.

One recurring issue is feature maturity mismatch. Capabilities are presented as if they are fully productized, while in practice they still depend on manual intervention, internal tools, special configuration, or senior engineers handling edge cases. This matters because the buyer may be underwriting margin improvement, product-led growth, or scalability based on capabilities that are not yet mature enough to support those assumptions.

Another common issue is untested scalability. A system may perform well at today's volume while hiding constraints that only appear under growth. The weak point may be the database, the reporting architecture, background processing, integration throughput, tenant isolation, or operational tooling. From the outside, the platform appears stable because current demand has not yet pushed it hard enough to expose the limit.

A third issue is key-person dependency, which is often harder to see than management dependency. Most deal teams know to ask whether the CEO, CFO, or head of sales is essential to the business. Fewer processes expose the senior engineer who understands the billing logic, the deployment pipeline, the legacy modules, the data import routines, or the customer-specific integrations that keep delivery moving. Nobody is eager to emphasize that dependency before close, because it weakens the story. After close, it can become one of the most urgent risks in the company.

The fourth issue is roadmap pressure. A roadmap can be directionally useful and still be unrealistic. If it does not account for technical debt, delivery capacity, quality problems, architectural bottlenecks, or the effort required to make existing features reliable, it may overstate what the business can achieve in the first year of ownership. A team already struggling to maintain the current platform will not suddenly absorb an aggressive expansion plan simply because the ownership structure changed.

Some of these issues are manageable with the right operating plan. Others should affect valuation, retention planning, remediation budget, or the pace of the post-close roadmap. The real danger is discovering them only after the investment thesis has already been approved.

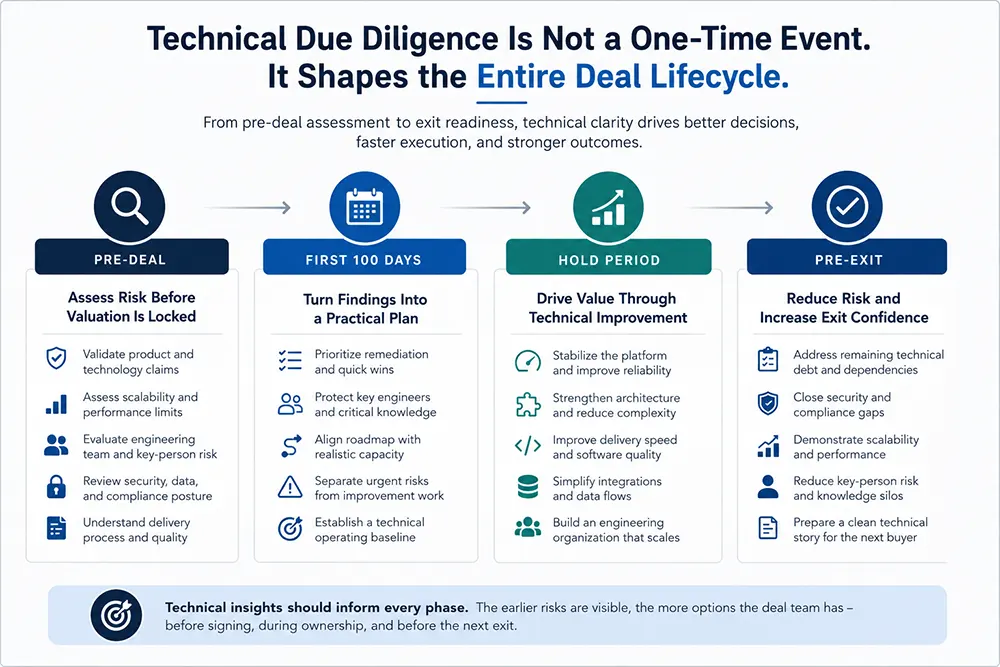

Technical diligence should become the ownership baseline

Technical diligence is most visible before close, but its findings should not disappear once the transaction is complete. If the work is done well, it becomes the first technical baseline of ownership. It helps the buyer understand what must be protected, what must be stabilized, and which assumptions in the growth plan depend on the platform improving.

In the pre-deal phase, the priority is to assess risk before valuation is locked. That means validating product claims, scalability assumptions, team depth, security exposure, data quality, and delivery reality. A long inventory of technical observations is only useful if it helps the buyer understand whether the system can support the commercial story being presented.

In the first 100 days, the same findings should turn into an operating baseline. This is where buyers often lose time, not because they have no information, but because the information is not translated into priorities. A useful diligence process should help the buyer decide what needs immediate remediation, which key engineers must be retained or supported, where roadmap expectations need adjustment, and which risks are important enough to deserve board-level visibility.

During the hold period, technical work should connect directly to value creation. Stabilizing the platform, improving release reliability, reducing delivery friction, simplifying integrations, strengthening architecture, and improving the engineering operating model may sound like internal engineering work, but the business effects are visible in revenue growth, margin, customer retention, and the company's ability to absorb scale.

Before exit, technical risk becomes visible again because the next buyer will ask many of the same questions. If fragile areas remain unresolved, dependencies are unclear, security gaps are still open, or the roadmap still depends on heroic engineering effort, those issues can affect confidence in the asset. Cleaning them up late is possible, but it is rarely as efficient as addressing them during ownership.

Handled this way, technical due diligence does more than support the pre-close decision. It gives the buyer a practical starting point for the operating agenda that follows.

Post-close pressure exposes what diligence only hinted at

Technical problems after close are expensive because they rarely remain technical. They begin to show up as slower delivery, missed roadmap commitments, customer escalations, higher support costs, security concerns, integration delays, and frustration between management, the board, and the engineering organization.

The instinctive response is often to increase management pressure through more reporting, tighter deadlines, and heavier process. That can help when the problem is poor execution discipline. It does very little when the platform itself is difficult to change safely.

A system with weak modular boundaries, poor automated testing, fragile deployment practices, unclear ownership, and hidden manual steps will resist growth. Adding engineers can increase coordination overhead before it improves output. Adding features can create more defects if the system is already difficult to change. Asking the team to move faster may increase operational risk rather than improve execution.

This is why technical findings need to be connected to investment consequences. Saying that the platform has technical debt is too vague to be useful on its own. Every real platform has technical debt. The more important question is whether that debt threatens the value creation plan.

Can the company support enterprise customers without major security remediation? Can it expand into multiple geographies without rebuilding assumptions in the data model? Can it introduce AI features safely, with proper data handling and production controls? Can the team ship the roadmap without spending the first six months stabilizing the platform?

Those are ownership questions, not engineering preferences.

The real cost is loss of control

The most damaging technical risks are not always the most dramatic. A complete outage is visible, urgent, and impossible to ignore. The more common problem is slower and harder to diagnose: leadership starts losing control over the pace and reliability of change.

Release dates become less predictable. Customer-specific workarounds multiply. Product managers stop trusting estimates. Engineers become cautious because every change carries hidden side effects. Support teams absorb complexity that should have been solved in the product. Leadership sees the symptoms, but it is not always obvious whether the cause is people, process, architecture, or some combination of all three.

This is where the investment thesis starts to bend. Growth may still be possible, but it becomes slower, more expensive, and more dependent on individual effort. The company may still hit revenue targets for a while, but delivery quality weakens underneath. The operating partner may notice the friction before the board sees the cause.

A good diligence process does not eliminate these risks. It makes them visible early enough to decide whether they are acceptable, whether they need to be priced, and whether the first year of ownership needs a different operating plan.

Technical diligence should not become flaw hunting

Good diligence should be practical, not theatrical. It should not look for reasons to criticize every shortcut or legacy decision. Real systems have compromises because real companies operate under deadline pressure, customer demands, staffing constraints, and changing product direction.

The work should distinguish acceptable operating debt from issues that change the economics of the deal. A two-week assessment will not uncover every problem, and it should not pretend to. Its purpose is to identify the risks that matter most before close, while the buyer still has room to act.

That may lead to a valuation adjustment, a different 100-day plan, a remediation budget, a retention plan for key engineers, a slower roadmap, or a decision to validate a platform assumption before committing to an aggressive growth target. In some cases, diligence may confirm that the platform is stronger than expected, which is also valuable because it gives the buyer more confidence in the investment thesis.

Finding technical issues before close is usually manageable. The more costly outcome is assuming they are manageable without knowing what they are.

What should be different after the review

A useful diligence review should leave the buyer with more than a list of risks. It should change how the first phase of ownership is managed.

If scalability was never tested, the 100-day plan should include controlled load validation before aggressive customer expansion. If key-person dependency is high, retention, documentation, and knowledge transfer should become immediate priorities. If AI features are immature, the roadmap should separate production-ready capability from demo-level functionality. If delivery is fragile, release reliability may matter more than new feature volume in the first quarter after close.

This is where technical diligence becomes useful to operating partners. It gives them an early map of where management attention should go and helps avoid treating every technical issue as equally urgent. Some risks need immediate action, some need monitoring, and some are acceptable as long as growth assumptions remain modest. There will also be issues that engineers care about but that do not materially affect the investment plan, at least not yet.

The goal is to give the buyer enough clarity to govern the risk without pretending the system needs to be perfect.

The cost of finding out late

A technical remediation program after close is almost always more expensive than a focused assessment before close. By then, the business is already operating under new expectations. The board wants progress, customers expect delivery, the operating plan is in motion, and the engineering team is trying to support the existing business while absorbing new demands.

That is a difficult moment to discover that the AI features are mostly prototypes, the platform cannot scale without database redesign, the roadmap depends on engineers who may leave, or the architecture cannot support the expansion strategy without major rework.

Technical due diligence does not eliminate risk. It makes risk visible early enough to price it, plan around it, or decide that it is acceptable. For PE firms buying software companies and software-enabled businesses, that visibility should not be treated as optional. It is part of understanding what is actually being acquired.

If you want an initial screen before a full review, start with the Due Diligence Risk Score Calculator.

Discussion Board Coming Soon

We're building a discussion board where you can share your thoughts and connect with other readers. Stay tuned!

Ready for CTO-level Leadership Without a Full-time Hire?

Let's discuss how Fractional CTO support can align your technology, roadmap, and team with the business, unblock delivery, and give you a clear path for the next 12 to 18 months.

Or reach us at: info@sharplogica.com